Aesop’s fable about the tortoise beating the hare provides a good analogy for investing. The trouble with investing is market noise. Investors generally know that with time they are likely to pick up a premium for owning equities relative to holding cash or bonds. Most investors know that time helps to turn bad short-term market outcomes into positive long-term outcomes. Most investors know that it is costly to buy and sell investments, incurring tax and transaction costs. Yet for all this evidence-based insight, investors still get spooked by the noise and uncertainty that they face in the markets.

What turns potential tortoises into hares?

But even so, many investors try to move their portfolios around, on account of short-term noise. It seems baffling why, but the answer lies in the way in which our brains are wired. We suffer a range of behavioral biases (immediacy, anchoring, loss aversion, overconfidence to name a few) that tend us towards being hares, rather than tortoises. These can be extremely costly. A recent piece of work in 2015 reveals that fund investors give up around 2% per year through trying to time when to be in and out of markets and funds. It also finds that investor looking to pick up the value premium (by owning relatively cheaper and less financially robust companies), give most of it up through poor timing.

‘On average, investors who invest in value mutual funds do not benefit from the excess returns reported by those funds because of the timing of their allocations… In fact, over periods with a documented high value premium, the average value investor in mutual funds has actually done worse than a buy-and-hold investor in an S&P 500 Index fund!’

It appears that the tortoise in them rightly seeks out value stocks, but the hare in them wants to get in and out to make more money.

The benefits of being a patient and dogged tortoise

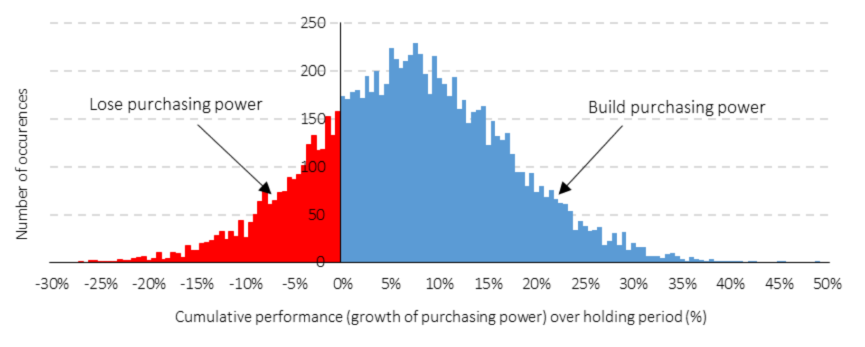

A recent piece of research provides us with a useful insight that clearly demonstrates the challenges of being a hare and the benefits of the patience and doggedness of the tortoise. It estimates the likely distribution of outcomes for a global 60% equity, 40% bond – portfolio based on a sample set of data from January 1975 to August 2016.

One can see that in the figure below that in any one-year period, a 60/40 global balanced portfolio has around a 1/3 chance of suffering a loss of purchasing power. Enough to make any hare jittery. The benefits of holding firm grow over time as the subsequent chart shows.

Figure 1: Annual cumulative real performance – the hare’s nightmare.

Note: 10,000 simulated 1 year periods using monthly data from the Jan 1975 – Aug 2016 data set. Source: Albion (2016).

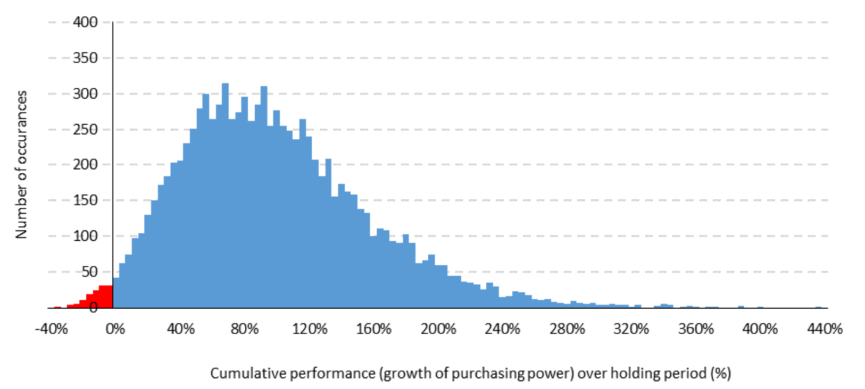

With a ten-year holding period (below), only a few investment outcomes do not deliver growth in purchasing power.

Figure 2: 10-year cumulative real performance – the tortoise nears the line.

Note: 10,000 simulated 10 year periods using monthly data from the Jan 1975 – Aug 2016 data set. Source: Albion (2016).

In conclusion

Holding firm is likely to deliver a successful investment outcome for the tortoise, without the activity and ultimate disappointment suffered by the hare.

Tips to help you win the race include avoiding looking at your portfolio too often, ignoring the news, and recognising that in the world of investing, activity is nearly always in surplus. And remember:

‘You may deride my awkward pace, but slow and steady wins the race.’ – Robert Lloyds ‘The Hare and Tortoise’, 1757. A Fable.

—

This post is a condensed form of our bi-monthly newsletter. To read the newsletter in full click here.

[1] Hsu, Jason C. and Myers, Brett W. and Whitby, Ryan J., Timing Poorly: A Guide to Generating Poor Returns While Investing in Successful Strategies (May 1, 2015). Available at SSRN: https://ssrn.com/abstract=2560434

[2] Albion Governance Update, October 2016 (in-house proprietary research)

[3] Proxy indexes are as follows: 40% global equity = MSCI World Index (net div.); 10% global value = Dimensional Global Large Value Index; 10% global small cap = Dimensional Global Small Index; 40% short-dated, high quality bonds = Dimensional Global Short-Dated Bond Index (hedged GBP), rebalanced annually, no costs deducted, but after inflation.

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.