It is unlikely that many readers of this blog will have noticed that the industry body that represents the fund management industry in the UK – The Investment Association – is in turmoil. By way of background, the Investment Association has over 200 member firms managing more than £5.5 trillion globally. Its aim is an honourable one: ‘to make investment better for clients, companies and the economy so that everyone prospers’.

Yet its CEO has just resigned, and two of the largest member firms – Schroders and M&G – are allegedly quitting the organisation because of recent reforms being undertaken. These reforms, delivered as a non-legally binding ‘Statement of Principles‘ to be signed by members, are aimed at aligning interests, placing clients first and providing investors with greater transparency on costs. Apparently only 25 out of 200 signed up! Every investor, surely, has the right to know what costs are being incurred to manage his or her money.

Every investor, surely, has the right to know what costs are being incurred to manage his or her money.

A recap on why costs matter

In order to understand the importance and impact of costs – and perhaps the reluctance of active managers to sign up to the new principles – one needs to understand that transacting in markets is a zero-sum game, in aggregate. The return of the market is simply the average return of all investors, before any costs have been deducted. In real life, the returns achieved by investors need to take into account the costs of transacting in the market.

The simple maths of the less-than-zero-sum-game-after-costs means that the average investor in lower cost passive funds will beat a majority of investors invested in higher cost active funds. That is a galling conclusion for the clever and hardworking active fund management community. Yet time and time again, the empirical evidence[1] suggests that the vast majority of active managers fail to deliver on their promise to beat the market.

The elements of investment cost

The range of fees and costs incurred by investors is long, complicated and hard to put an accurate figure on, something the Investment Association’s ‘Statement of Principles’ would have done much to improve. We have a go.

Investors are, by-and-large in the dark when it comes to dealing costs.

Ongoing Charges Figure (OCF):

The ongoing charges figure (OCF) is the overt cost that investors incur by investing in a fund. This is the sum of the Annual Management Charge (AMC) charged by the fund manager and the other direct costs incurred by the fund, which can be offset against the fund’s performance. As such, the OCF is nearly always higher than the AMC alone. OCFs can be found in the Key Investor Information Documents (KIIDS) that each fund or ETF is required to produce.

Turnover (dealing) costs:

These are the covert costs incurred by investors when securities within a fund are bought and sold. The costs are the product of the proportion of the fund that has been turned over and the costs of transacting the trades to sell and buy securities. Investors are, by-and-large in the dark when it comes to dealing costs.

Costs in practice

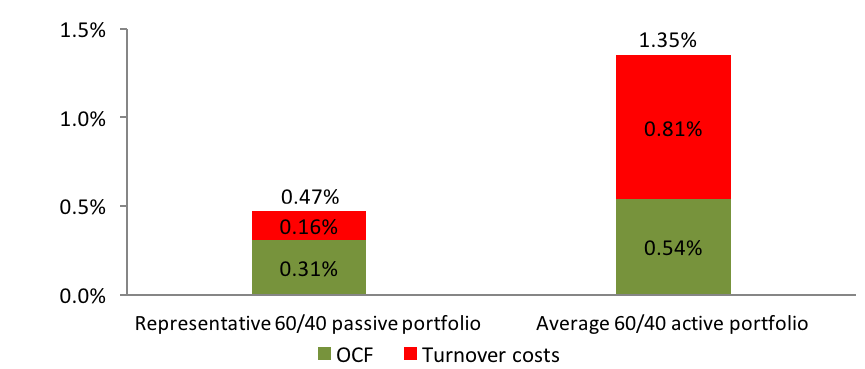

The figure below provides a summary of the estimated cost differential based on the latest research that we can find, capturing both the seen and hidden costs. The figures relate to a 60% growth assets (equity) and 40% defensive asset (bond) mix. The representative passive portfolio is based on a global portfolio with allocations to value and small cap equities, emerging markets and global commercial property, balanced by short-dated global bonds and inflation linked bonds. The average active portfolio is based on the same asset allocation and dealing costs, but uses average OCFs of UK domiciled equity and bond funds and sector specific turnover rates.

Figure 1: Cost comparison – costs matter

Conclusion

It is impossible to overstate how important it is to manage costs of all kinds tightly. It is something that we continue to do on behalf of our clients, through our systematic, low cost approach to investing. Over the past few years passive fund costs have fallen significantly, which is great news for investors. As the legendary Jack Bogle[2] once said:

“In investing, realize that you get what you don’t pay for. Whatever future returns the markets are generous enough to deliver, few investors will succeed in capturing 100% of those returns, simply because of the high costs of investing—all those commissions, management fees, investment expenses, yes, even taxes—so pare them to the bone.”

We agree.

—

Note: this blog post is a condensed form of the full newsletter, Smoke, Mirrors and the True Cost of Investing.

[1] For example[2] In Investing, You Get What You Don’t Pay For. Remarks by John C. Bogle, The World Money Show February 2, 2005, Orlando, Florida

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.