All investors know that they need to take risks in order to achieve returns higher than cash. If you asked ten investors if equities were more risky than cash, most would agree; but that depends on how one understands risk. The investment industry has done a poor job of explaining risk as it relates to an investor and tends to equate risk with return volatility. William Bernstein – a neurosurgeon-turned-adviser and prolific investment writer – wrote a great, short booklet on risk1, where he explained the different risks that equity investors face, as follows:

‘Risk, then, comes in two flavors: “shallow risk,” a loss of real capital that recovers relatively quickly, say within several years; and “deep risk,” a permanent loss of real capital.’

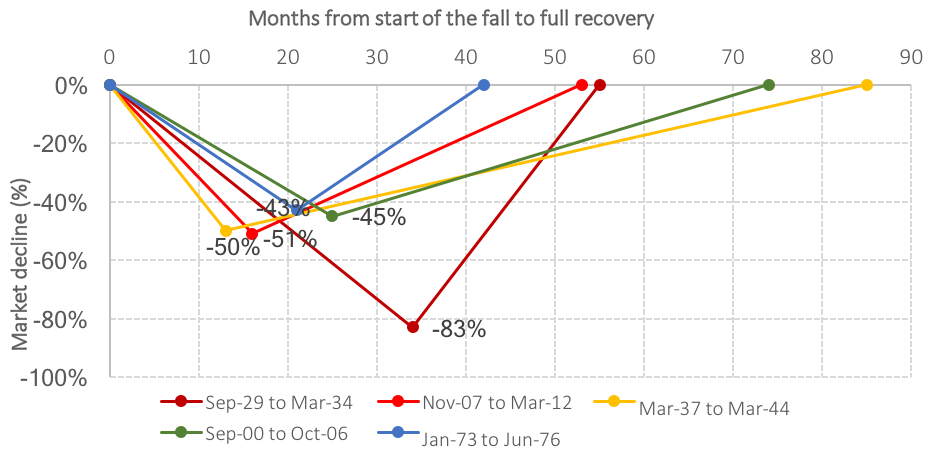

Shallow risk – precipitous equity market crashes that recover relatively quickly

This first level of risk is the one that most investors focus on, yet is perhaps the least relevant, particularly for those with long investment horizons. These are the scary and emotionally fraught times when equity markets fall dramatically, the latest example of which was the Credit Crisis of 2007 to 2009. We illustrate below, the five largest equity market falls in the US market, since 1927 (in US$ terms).

Five largest falls in the US equity markets between 1927 and 2017.

Data source: Ibbotson SBBI US Large Stock TR, Jan-25 to Apr-17. Morningstar © All rights reserved.

Deep risk – a permanent loss of wealth

Bernstein defines deep risk as the permanent loss of purchasing power on account of four events: hyperinflation, such as that of the Weimar Republic, where from 1921 to 1924 bonds and cash lost nearly all their value; prolonged deflation causing a depression and high unemployment; devastation i.e. wars and geopolitical events, such as the Bolshevik revolution (almost 100 years ago to the day) resulting in the closure of the Russian stock market and default on Tsarist government debt; and finally confiscation, which still happens today e.g. the Argentinian government’s expropriation of the Spanish oil company Repsol’s assets in the country in 2012.

There are two investment behaviours that translate shallow risk into deep risk. Being shaken out of the market by a precipitous rapid fall (shallow risk) and then failing to get back in again – as there never seems to be a good time to do so – crystallises a real loss (deep risk). Owning concentrated stock portfolios can do the same; a recent study2 in the US shows that 26,000 listed companies have been in and out of the US equity exchanges since 1926, with a mean life of only seven years. Only 36 companies have made it through from 1936. Owning high exposures to stocks that fail is deep risk.

The best mitigants of deep risk are to own a globally diversified portfolio of several thousand stocks distributed predominantly across developed equity markets of democratic countries with a sound legal framework. Equities provide the prospect of strong, long-term inflation-plus returns.

In conclusion

Investors know that placing money in the bond and equity markets carries risk. Yet the way in which many look at, and measure, risk is disconnected from investors actual longer-term investment horizons, focusing on shallow risk, rather than deep risk. Unless one understands the probability of an adverse event (hazard) happening and the effect of this exposure, due to a specific hazard on the individual investor, then it is likely that the real risks faced by an investor are masked by the shallow risks that have more emotional impact. Owning more ‘low risk’ bonds (or cash) is not necessarily always the right answer when trying to avoid the deep risks that investors face.

—

This post is a condensed version of our June 2017 Newsletter, which you can read in full here.

1 Bernstein, W.J., (2013), Deep Risk: How History Informs Portfolio Design. Available at www.amazon.co.uk.

2 Bessembinder, Hendrik, Do Stocks Outperform Treasury Bills? (May 22, 2017). Available at SSRN.

This article does not constitute financial advice. Individuals must not rely on this information to make a financial or investment decision. Before making any decision, we recommend you consult your financial planner to take into account your particular investment objectives, financial situation and individual needs. Past performance is not a guide to future performance. The value of an investment and the income from it may go down as well as up and investors may not get back the amount originally invested. This document may include forward-looking statements that are based upon our current opinions, expectations and projections.